Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

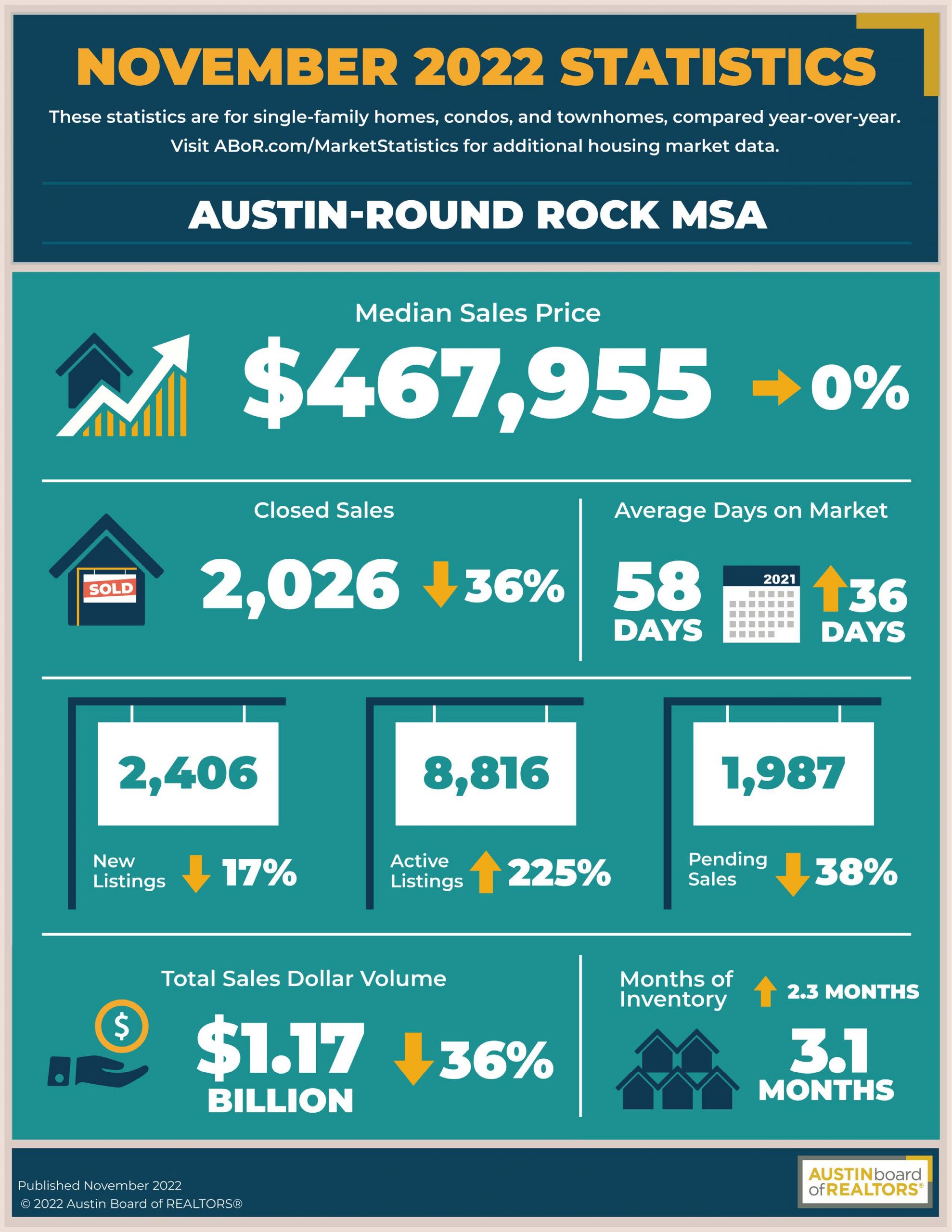

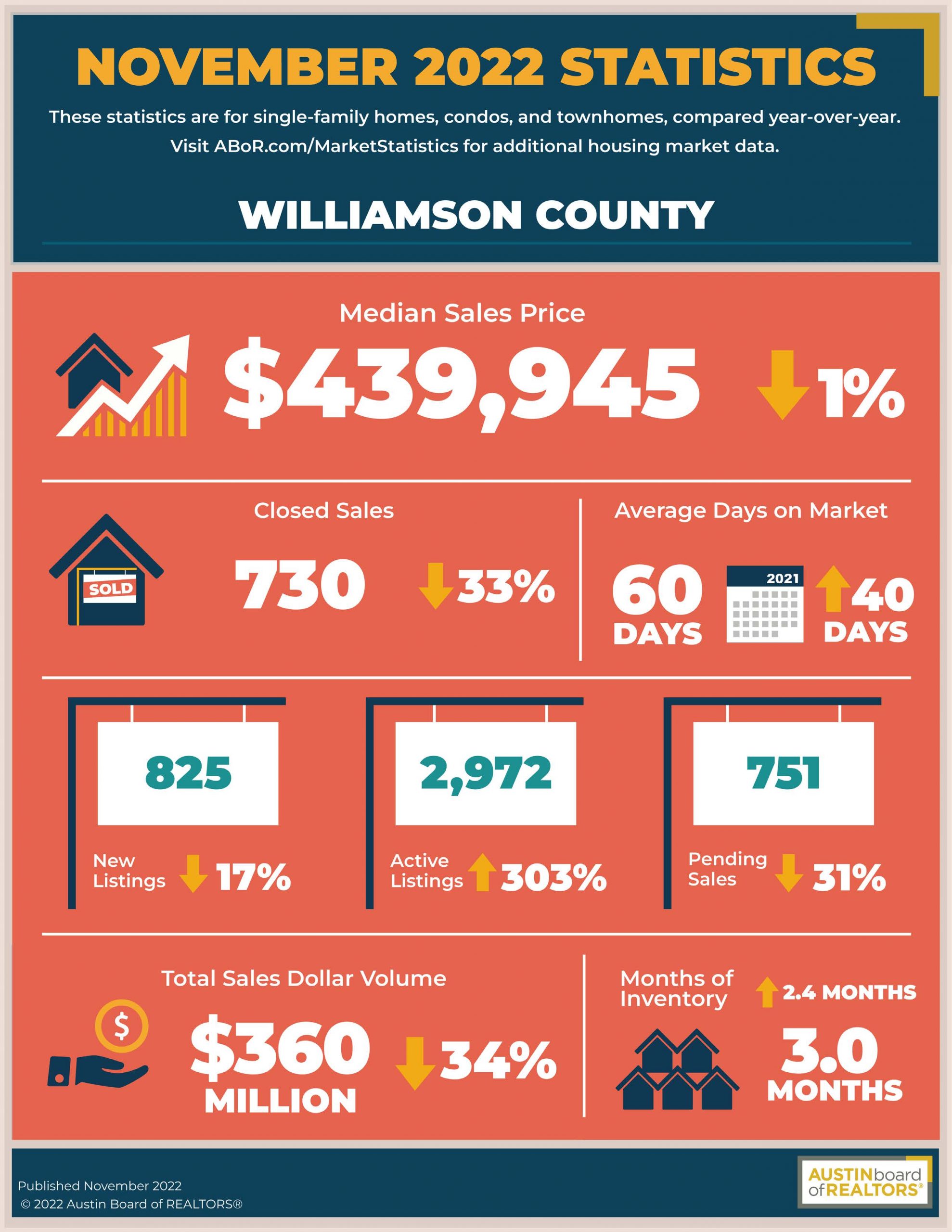

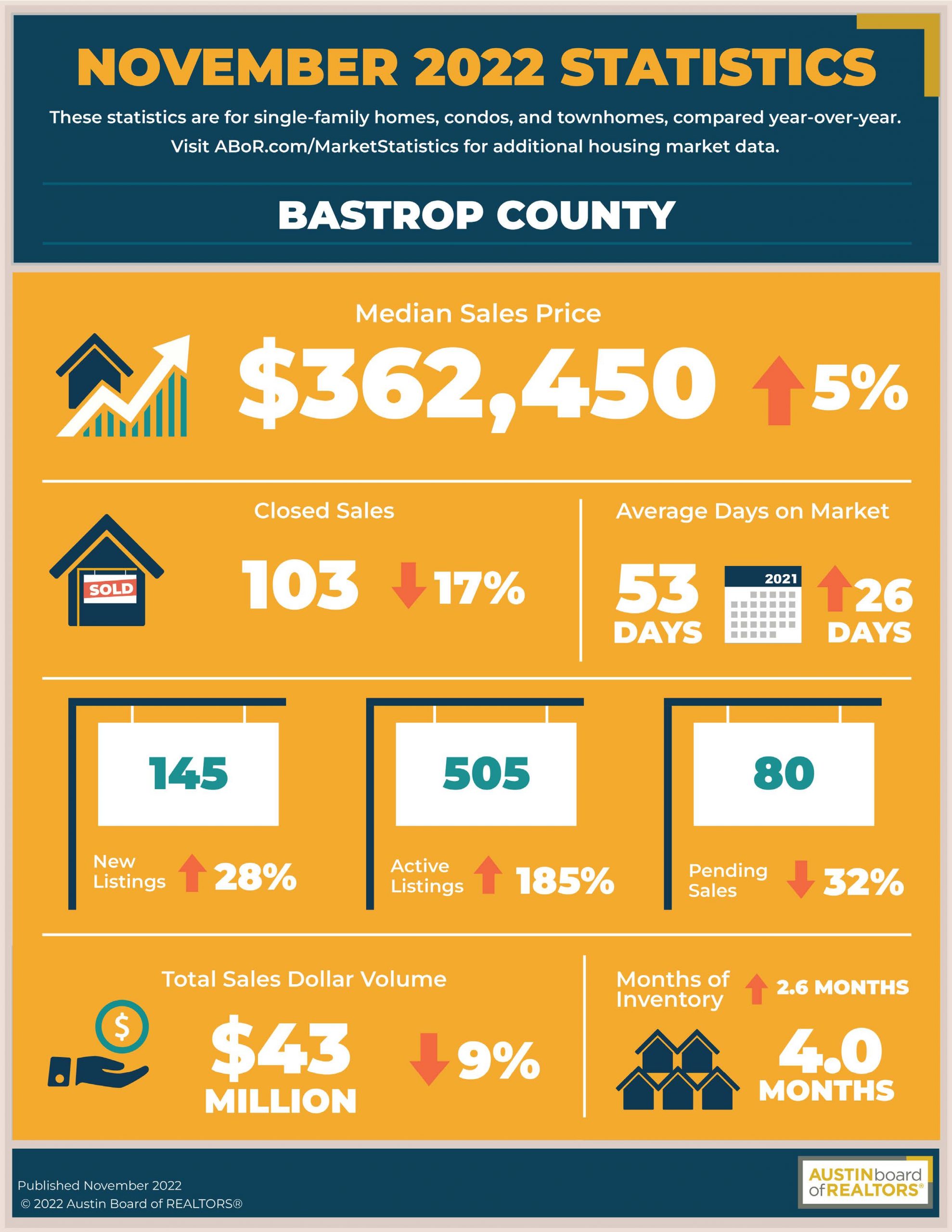

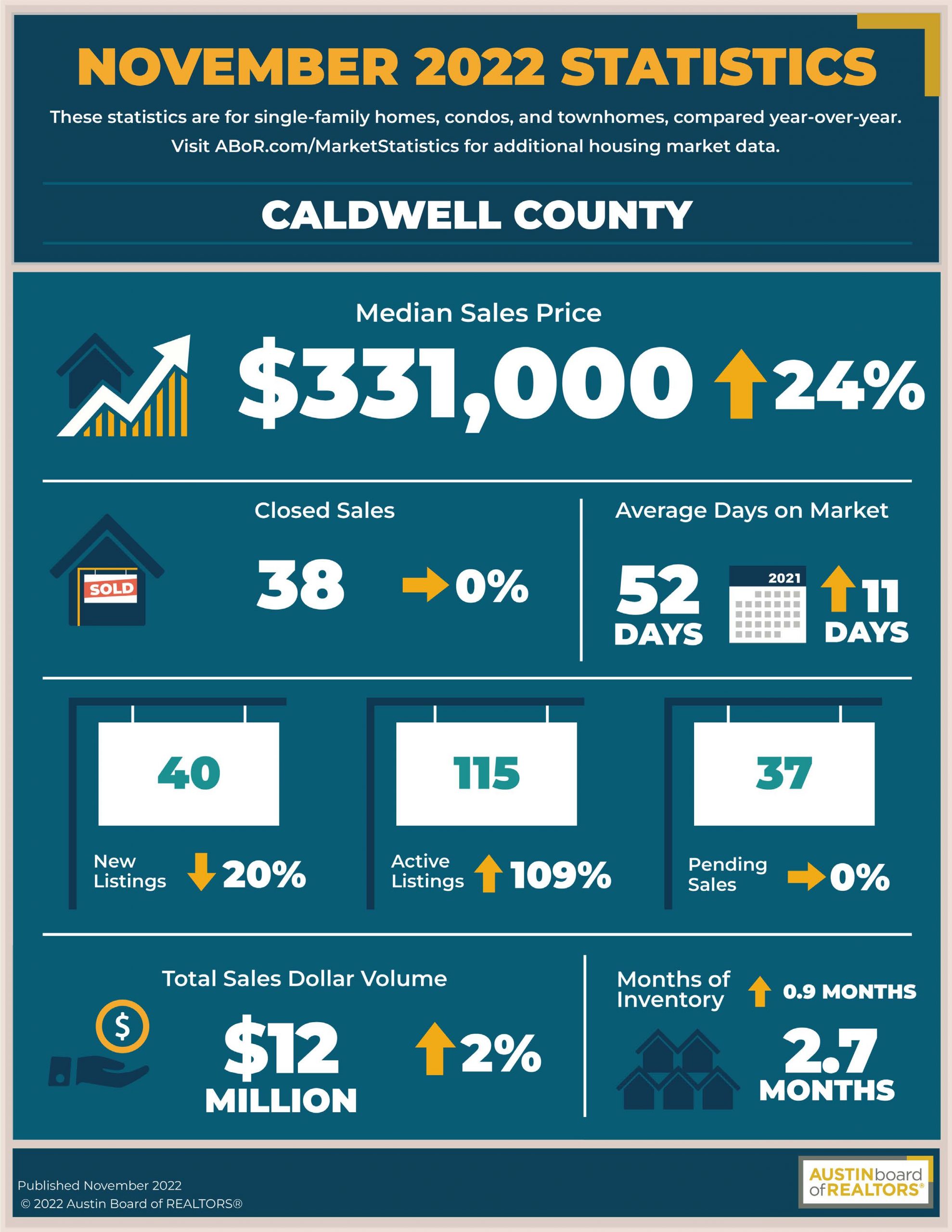

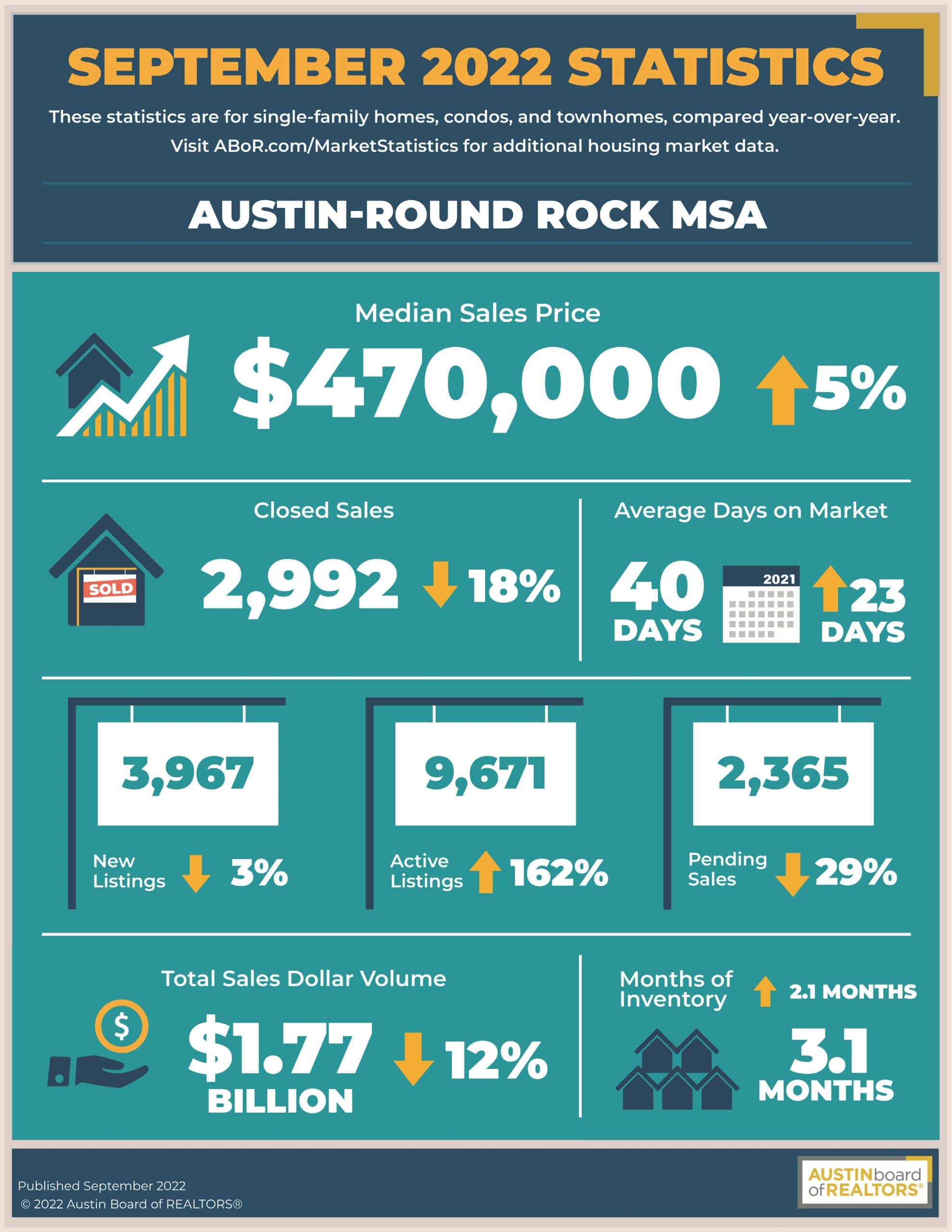

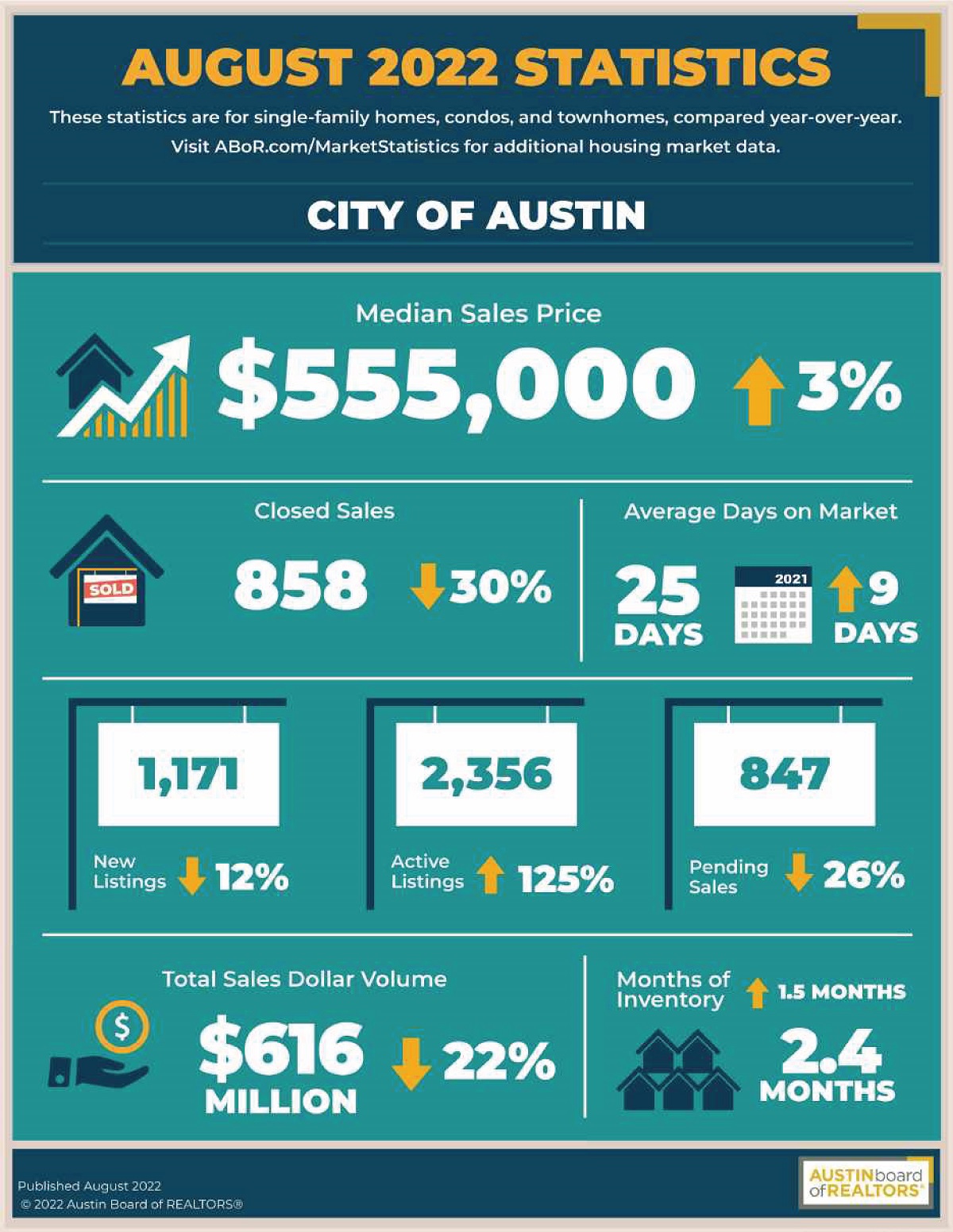

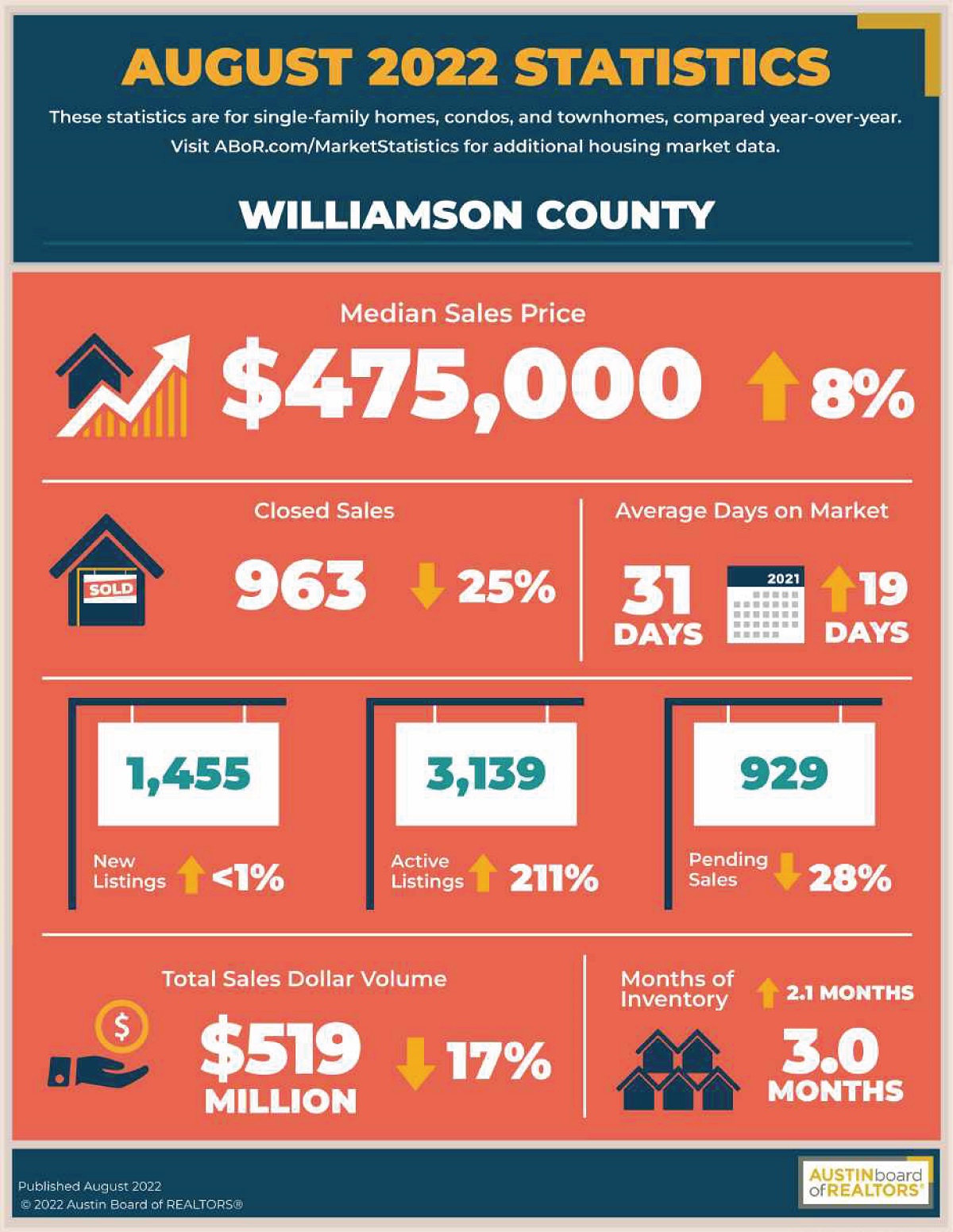

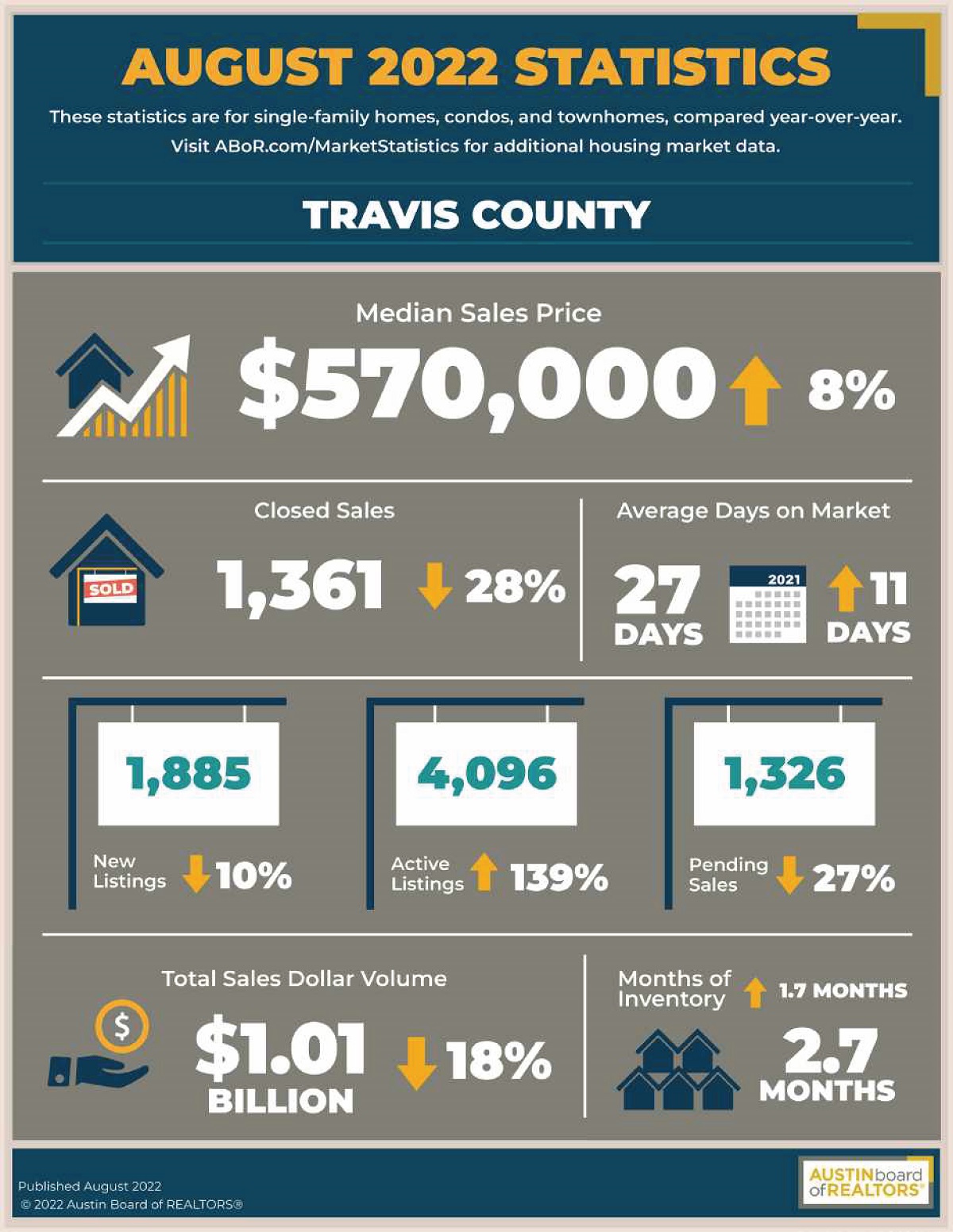

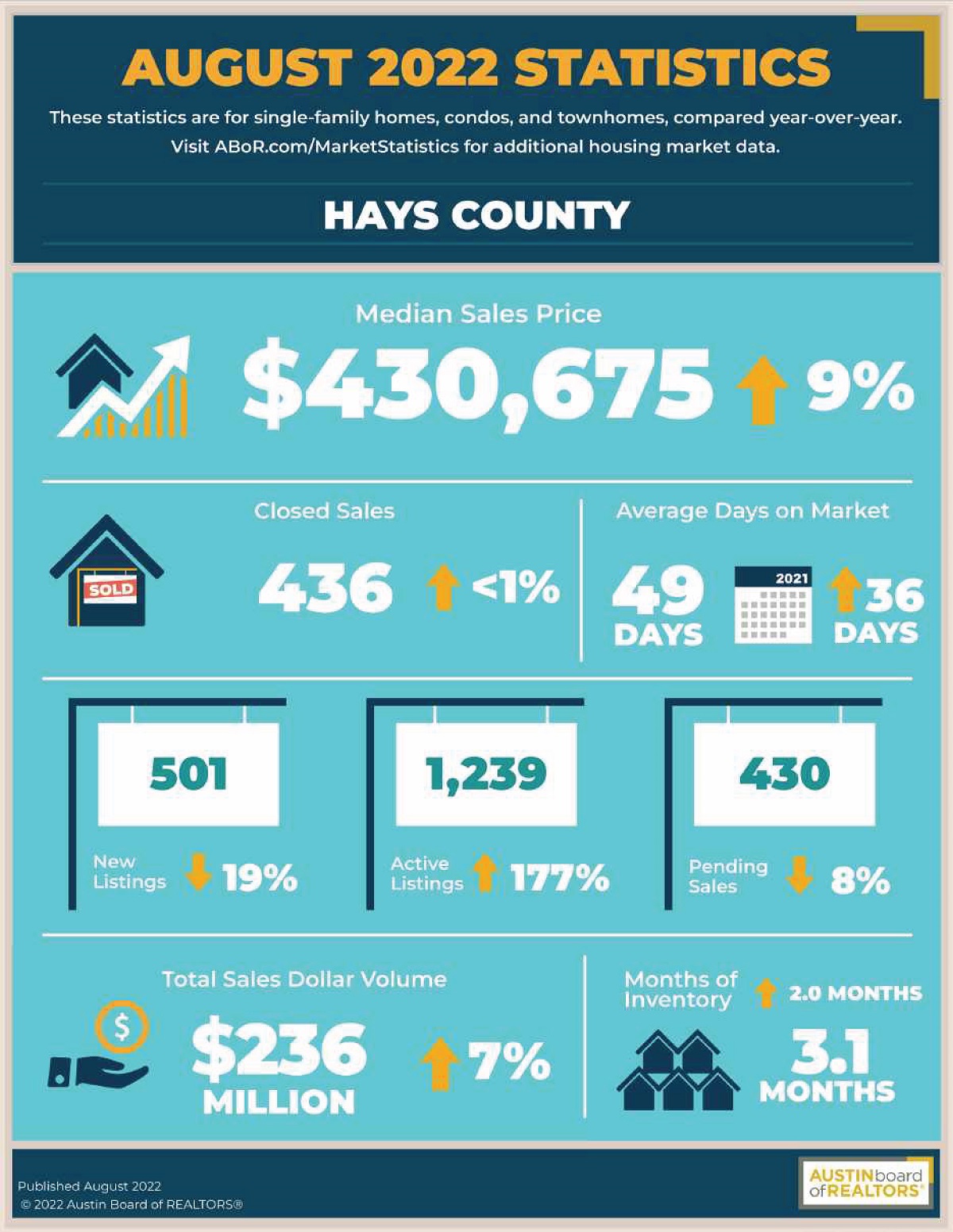

ABOR: Median price for a home in Austin-Round Rock MSA stays flat, no sales or price records set. November housing inventory nearly quadruples.

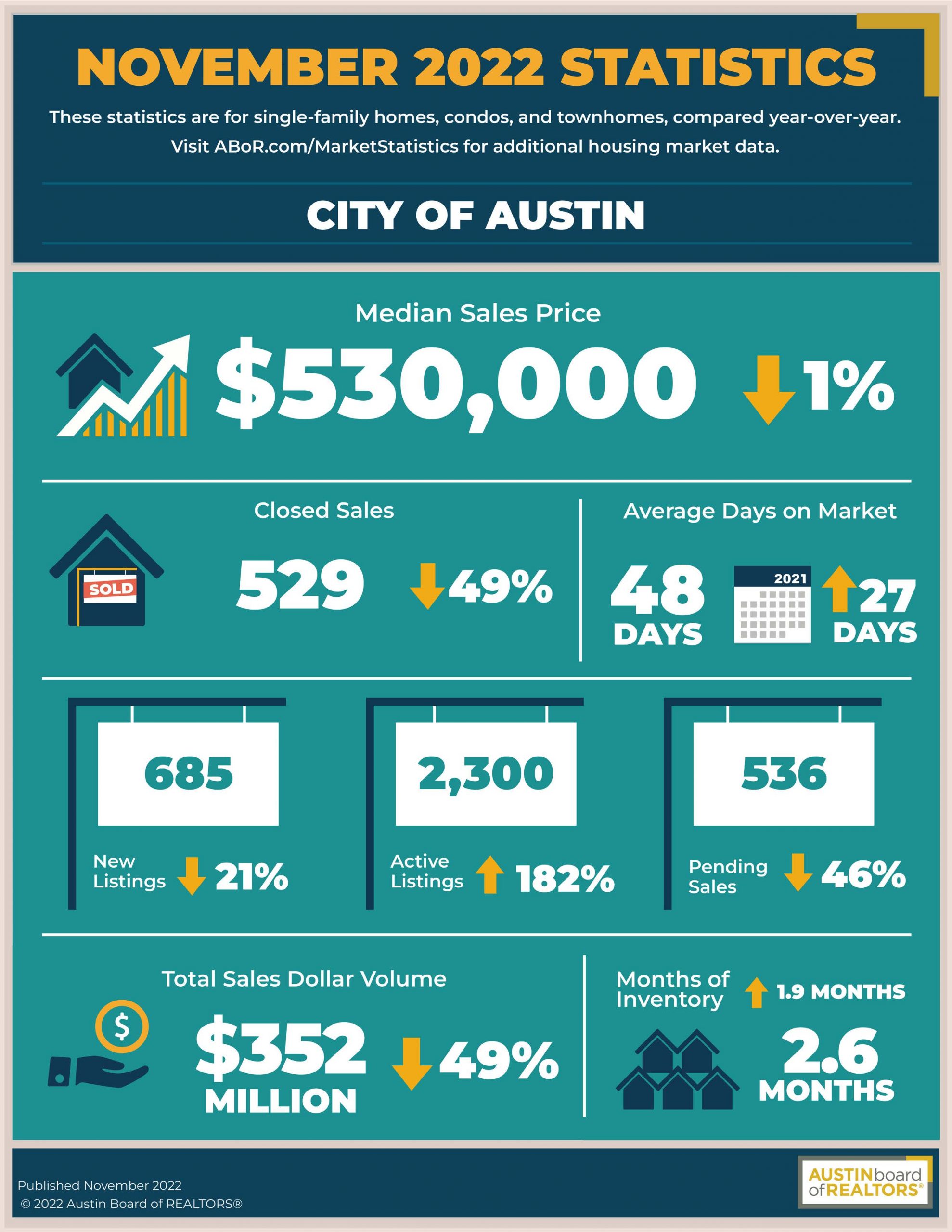

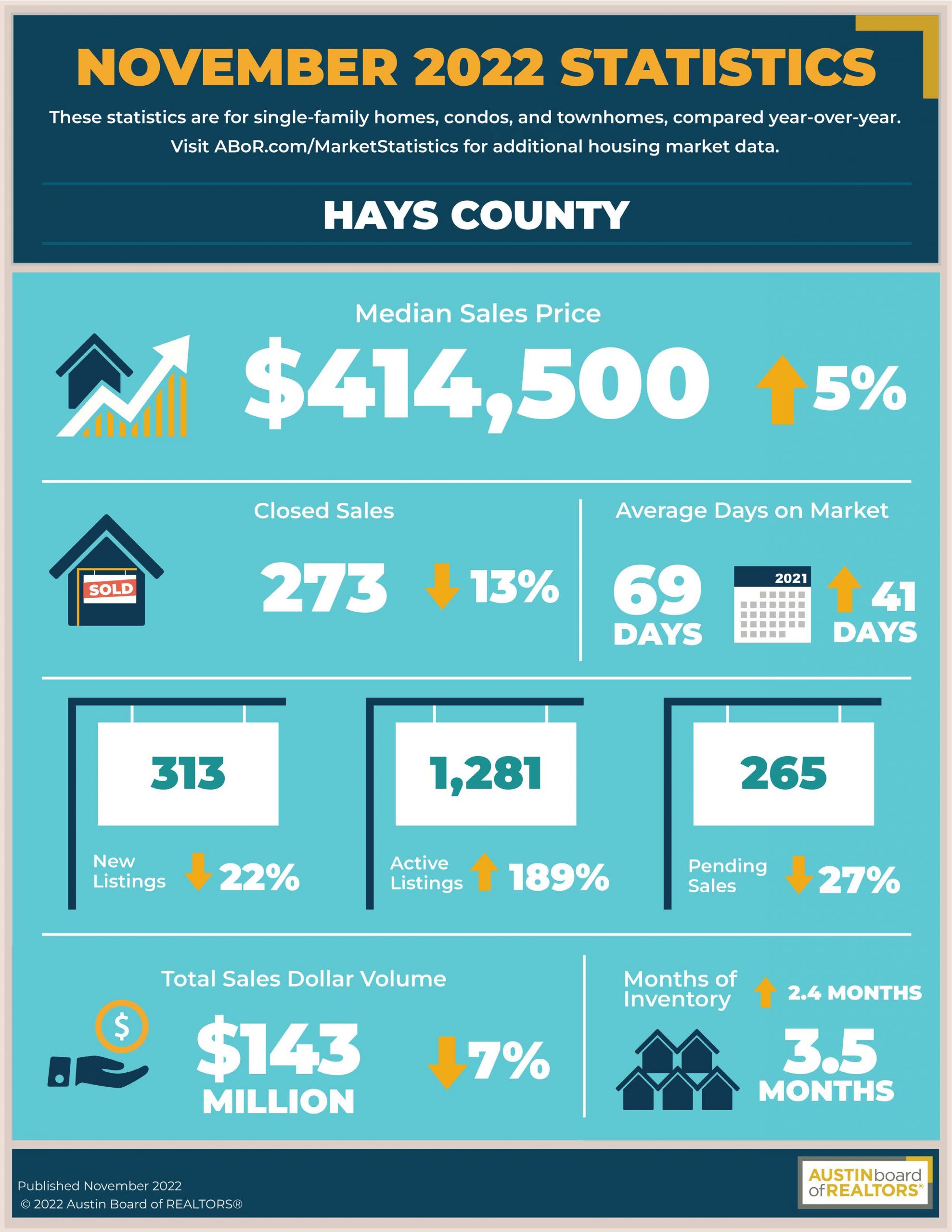

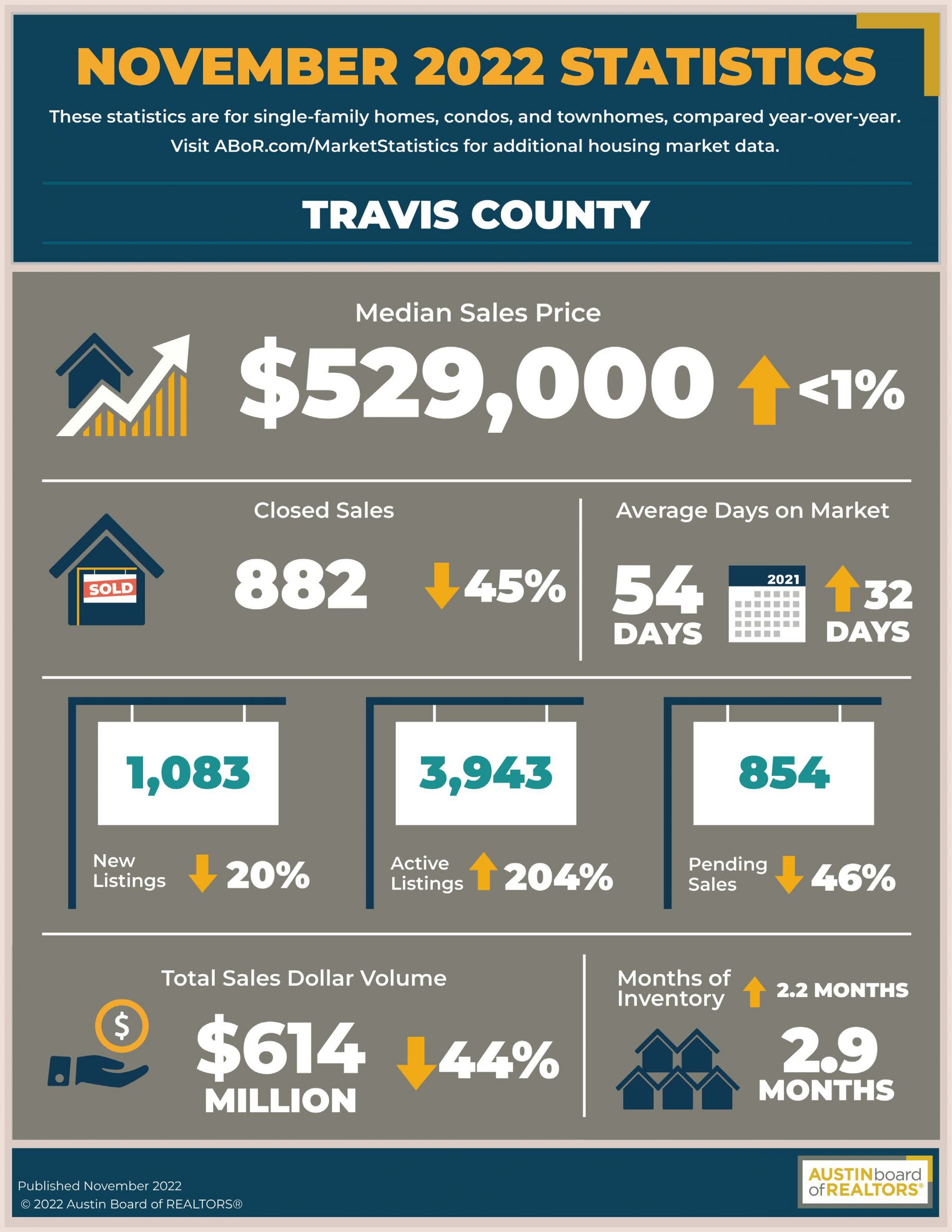

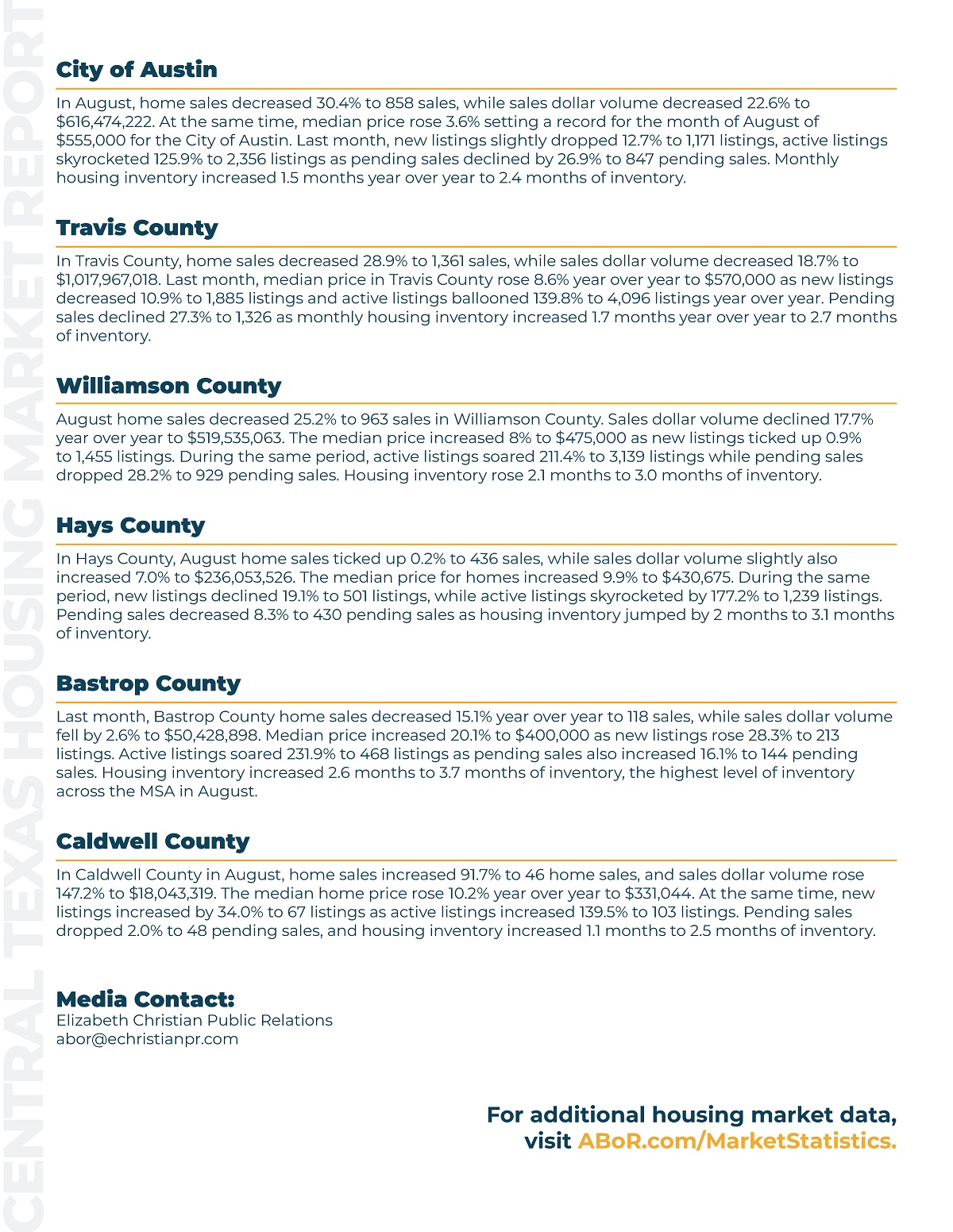

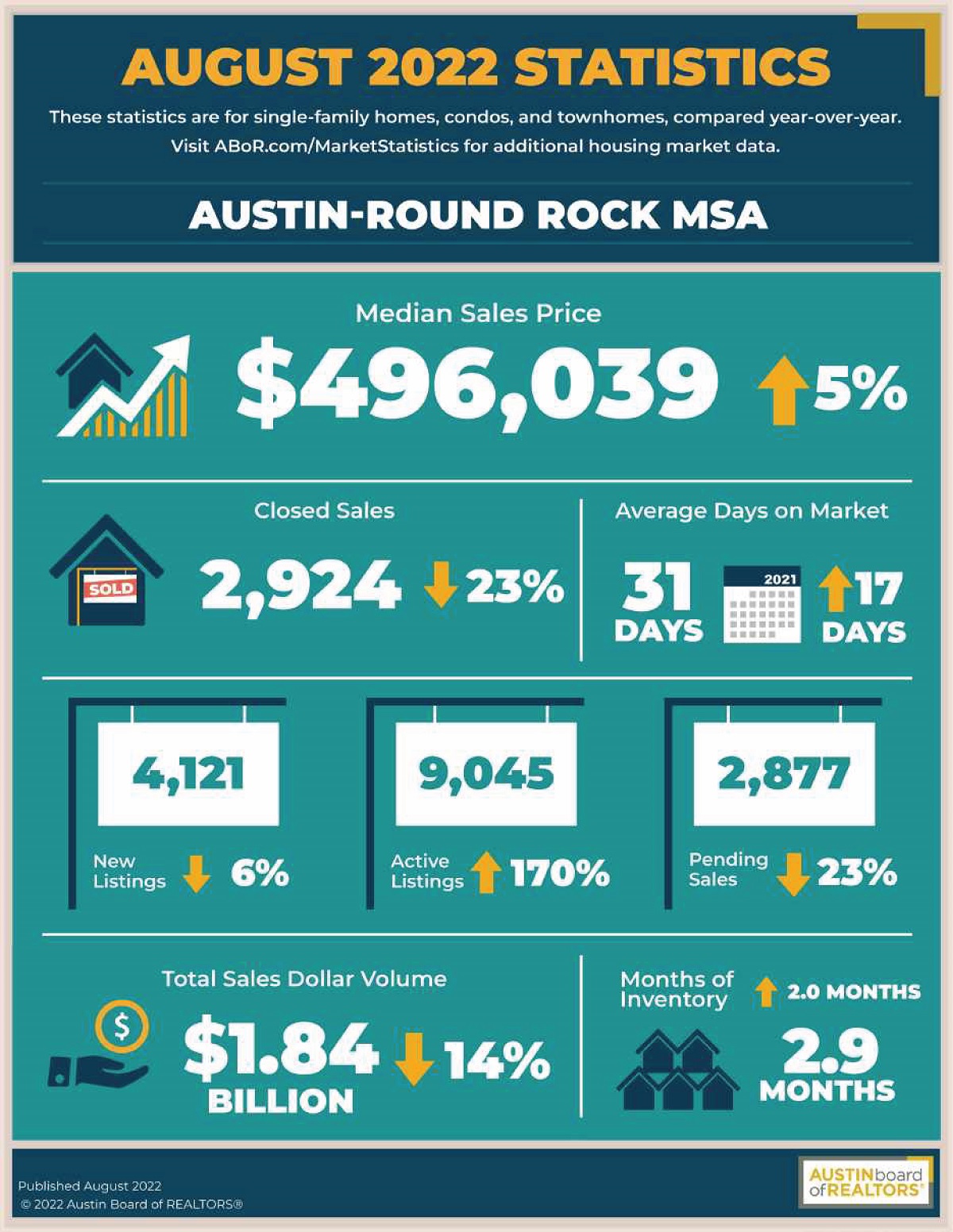

AUSTIN, Texas —For the first time since February 2019, median home prices in the Austin-Round Rock MSA experienced a 0% year over year increase, according to the Austin Board of REALTORS® November 2022 Central Texas Housing Market Report. As housing inventory and days on the market continue to steadily increase across the MSA, the report indicates normal market activity could be here to stay, as Austin’s housing market maintains its trajectory toward balance and sustainability. For the first time since the spring of 2020, there were no records broken for home sales or median price in either the MSA or City of Austin.

“It’s a relief to see more homes available and sitting on the market long enough to give buyers an opportunity to think before they leap,” Cord Shiflet, 2022 ABoR president, said. “This healthy competition creates an opportunity for homebuyers, who may have struggled within the past two years, to take their time and find a home they love. At the same time, sellers who can still enjoy deep equity should connect with your REALTOR® to discuss the best way to prepare and market their home.”

Last month, home sales declined by 36.6% to 2,026 closed listings— the largest drop in closings by percentage since May 2020 during the initial COVID-19 economic hesitancy when closings fell 29.2%. Sales dollar volume fell by 36.8% to $1,175,435,108 as new listings declined 17.8% to 2,406 listings across the MSA. Pending listings dropped by 38.3% to 1,987 listings and available inventory increased by 2.3 months to 3.1 months of inventory. Homes spent an average of 58 days on market, up 36 days from November 2021.